Netflix’s Tiny House Nation is a TV show I enjoy tremendously because the idea of transforming the smallest space into the most functional and beautiful homes is just mind-blowing. It also reflects a growing movement that believes in simple living. What’s not to like about spending a lot less time cleaning?

It’s part of the minimalism movement, which I think is not only about reducing stuff but also about prioritising essentials. You become more conscious of the things around you instead of just consuming, so the earth will thank you for reducing your carbon footprint. This might sound a little new-agey but if it results in more money in your pocket and happiness, why not?

Changing the narrative on renting

Renting your home has shades of minimalism. If renting is generally cheaper than buying, the reduced cash flow needed to secure a roof over your head results in more money available for investing and opens up other possibilities in life. So it might be time to have a new way of thinking about property as well as upgrading the financial considerations.

Right off the bat, I should clarify that I’m not trying to force you to take the side that you must rent. Rather, I want to propose an alternative to our cultural fixation that you must buy a property, especially in the face of “severely unaffordable” homes.

First, let’s acknowledge the advantages of buying a property:

- Leverage and asset accumulation. Leverage is the ability to borrow, and real estate is an asset the bank doesn’t mind lending you a lot of money to buy because it’s generally an appreciating collateral. If you fail in your mortgage obligations, the bank can easily sell the property to recover any losses. All you need to do is pony up a relatively small sum and presto! you own a very expensive asset. After 30 years, a property costing RM500,000 appreciating at 5% every year will be worth about RM2.2 million.

If you’re a speculator, leverage gives you a huge short-term profit from a small price appreciation. But you could also lose your pants if the reverse is true.

- Inflation protection. Rentals are exposed to inflation because landlords pass on rising property values to their tenants. But as a property owner, your fixed mortgage payments for the loan’s duration becomes cheaper and cheaper after adjusting for inflation. After the loan is paid off, you live in your home for “free”.

- A sense of security. No landlord will be able to evict you. You do as you wish to your home, including renovating it to your tastes. You live in the neighborhood for the long-term, forge close bonds, and are part of the local community. Your home is a very tangible asset added to your name, which might become useful security if you needed to borrow money for other emergencies.

- Estate Planning. Buying a home could be a good way to establish an estate, especially when bought with an MRTA (Mortgage Reducing Term Assurance). This is an insurance policy which pays the mortgage fully if the homebuyer dies unexpectedly. The home goes to the family debt-free posthumously. Without an MRTA, a home that has gone up in value will still be passed on to beneficiaries but the bank will still be owed the loan’s remainder.

Now, let’s discuss the advantages of not buying a property:

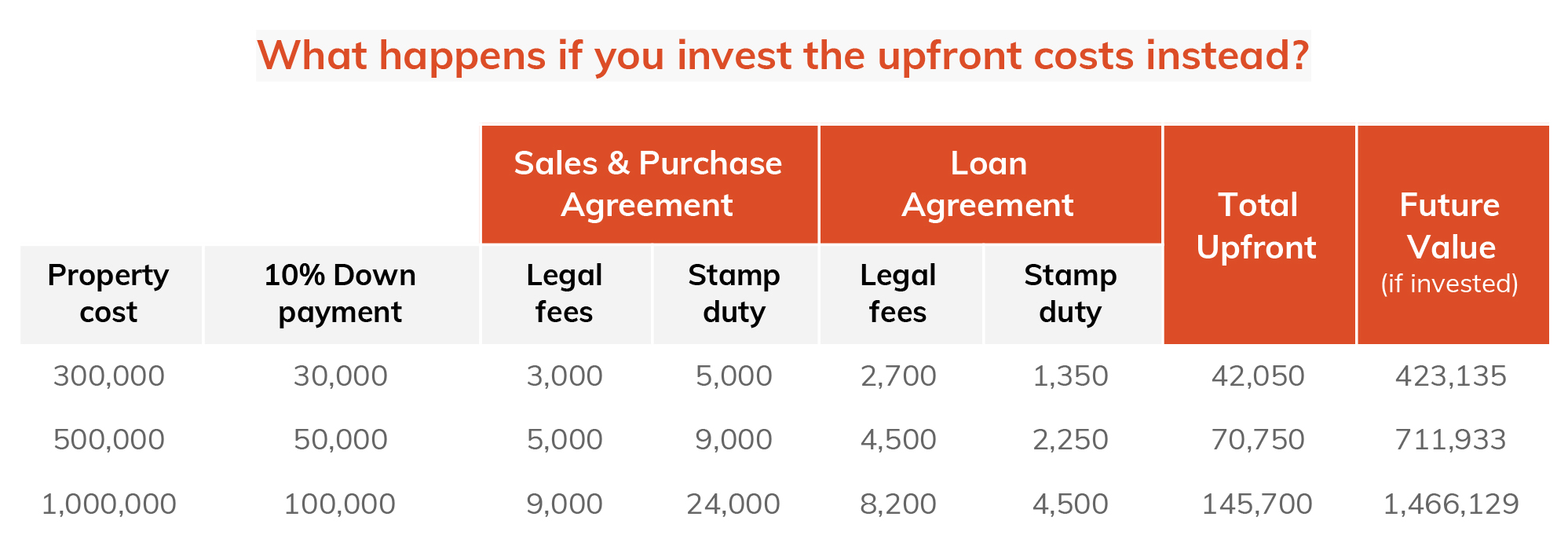

- You could invest the huge upfront cash needed.

There are a lot of hidden costs when it comes to buying a home. The major ones are legal fees and stamp duty. The downpayment is technically not a cost, but you’d need to cough up this sum because your bank isn’t going to give you 100% financing (not yet anyway). All this comes up to quite a bit, which if invested could also balloon to quite a bit.

For example, investing the upfront cash needed for a RM500,000 property will give a projected value of more than RM700,000 30 years later (the assumed timeframe for the housing loan).

Assumptions:

Return rate: 8%

Loan tenure (or investment timeframe): 30 years

Calculator source: Loanstreet

- You could invest the difference between rent and instalment payments.

Rentals seem to be very sticky. Having been both landlord and tenant myself, this seems to be the experience. Despite what we said earlier about inflation, landlords seem to be nice people who raise the rent only once every few years. (Maybe there are too many empty homes.) Slow-rising rents give renters more opportunities to save money, which nudges them closer to or ahead of owners in the investing race.

An example of the investment potential when you invest the difference between installments and rent:

• Landlord’s property value: RM500,000

• Landlord’s installment: RM2,280 (Source: Loanstreet)

• Renter’s rent: RM1,500

• Difference: RM780

• Portfolio value at 8% p.a. 30 years later: About RM1.2m

This really depends on the business cycle, location, and your rental preference. Ideally, you should compare the home you want to rent to the same type of home you’re thinking of buying. But if that’s too aspirational because your desired home is too expensive to buy or even rent, you could try the minimalist path and rent a cheaper home. Forcing yourself to save whatever the notional buy-rent difference gives you more room for asset accumulation. Either way, be nice to your landlord and pay your rent on time.

- Renting avoids ownership hassles.

A buyer would have to spend substantial amounts on renovation and furnishing. Depending on your preferred lifestyle, this could range from RM25,000 to RM50,000 in costs for a RM500,000 property. Investing this over a period of 30 years could give you a future value of RM250,000 to RM500,000. Owners also have to pay for repairs and maintenance (which, you guessed it, could instead be invested). But how much does it cost when a pipe leaks in a rented home? Just call the landlord.

- Renting gives you flexibility.

Millenials have been called “The Job-Hopping Generation”. Spin it positively and you could say they’re not afraid of embracing job-hopping for career advancement and satisfaction. The advantage that stands out, whether you’re a fickle job-hopper or just an occasional career-enhancing job-seeker, is that renting gives you the proximity option (notwithstanding the new normal of working from home).

The huge qualitative factors that come out of this include savings on transportation costs and longer sleeping hours. Ultimately, it’s also liberating not being ball-and-chained to a lifetime of debt. Thinking of that sabbatical in a local seaside village to discover yourself? Just pack up and go.

- Renting gives you liquidity.

Continuing with the flexibility theme, you can’t sell a property one brick at a time to fund your lifestyle. But a renter with a solid portfolio could sell just enough to provide for immediate cash needs, while also allowing the portfolio to continue growing. This is useful for both long-term needs like retirement or short term ones like a holiday. On the other hand, this would be a lot more challenging and costly for owners. A refinancing could, for example, be taken out on a property loan but that would incur expensive legal and administrative costs.

Don’t rule out renting just yet

When you consider the question both financially and qualitatively, it’s a close race between renting and buying when it comes to asset accumulation. But the allegation that a renter “would be left with nothing” or that “money is wasted on rent” should forever be consigned to the dustbin of silly financial arguments. In short, there’s no one-size-fits-all solution, but there are now serious options for getting around affordability or debt issues and the stress that comes with that.