Year-To-Date 3rd Quarter 2022 Market Review

So far in 2022, stubbornly high inflation, steep interest-rate hikes, recessionary worries, conflict in Europe, and the soaring US Dollar triggered severe asset-price volatility. The headwinds appeared to wane in July and August. However, markets were under pressure in late September as central banks continued tightening policy as inflation remained high and weaker than expected economic growth. But investors remained worried about high inflation, slowing economic growth and the potential cause of recession if for Fed raised interest rates too aggressively an aggressive Fed to cause a recession. The only source of comfort is that investor sentiment is very negative, and valuations provide the margin of safety, providing some reassurance that markets have already accounted for the bad news.

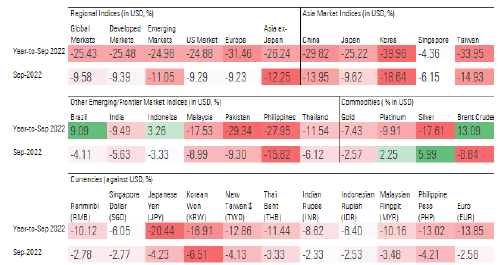

Performance of Major Indexes, Currencies, and Commodities

<Source: Morningstar Direct Data as of 30 June 2022 (Regional and market indices were based on the respective Morningstar total return index. Gold and platinum prices were based on the LBMA Price PM; silver price was based on the LBMA price.>

The US, Developed ex-US, and Emerging markets declined about 25% over 3 quarters. Rather than diversifying stock losses as seen in 2020, 2008 (Global Financial Crisis) and 2000-02 (Dot-Com Bubble followed by 9/11 and recession), bonds have plunged too. Rising interest rates have sent yields soaring and prices into freefall. The Morningstar US Core Bond Index and Global Treasury Bond Indexes were down 14% and 23% in 3 quarters.

Currently, the Morningstar US and Global ex-US indexes look more attractive based on P/E, dividend yield and Morningstar equity research-assigned valuation.

The US Dollar has benefited from Fed hawkishness and its safe-haven appeal during market volatility. In real trade-weighted terms, the US Dollar is the strongest since the Piazza Accord era of the mid-1980s.

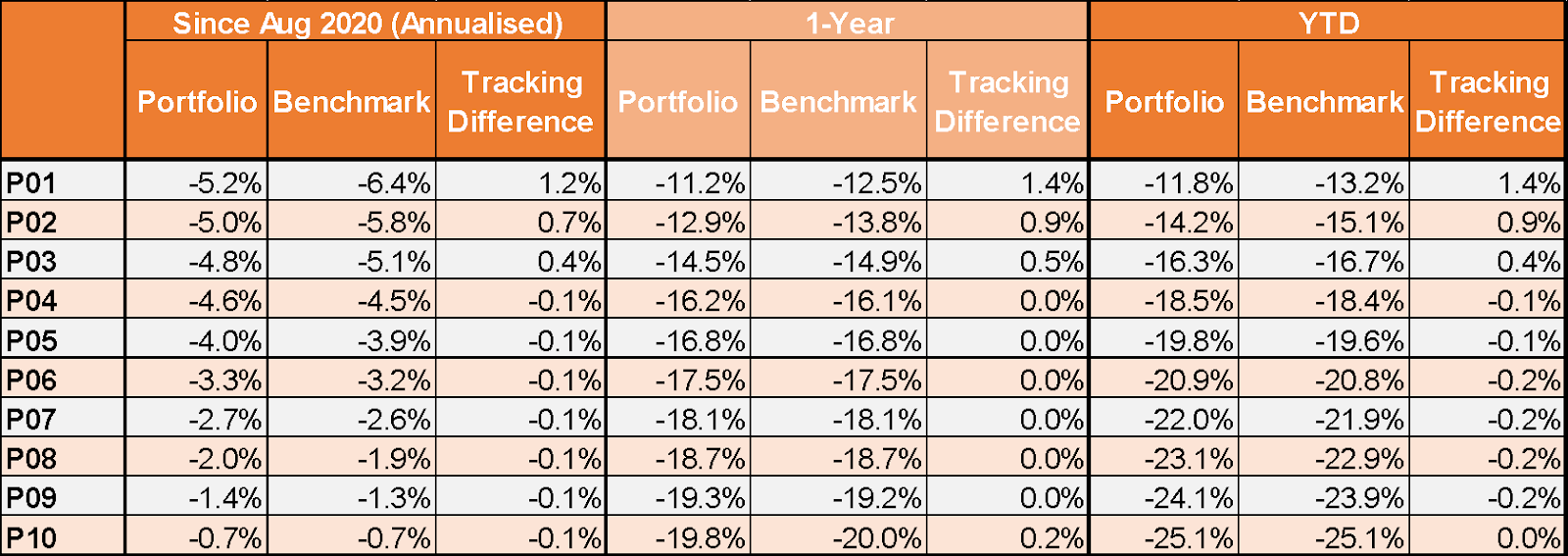

Portfolio Performance As of September 2022

Total Returns in USD

<Source: Morningstar>

The annualized returns for P04-P10 continued to track its underlying benchmark closely. As for P01-P03, outperformance was due to slightly better returns in Malaysia's fixed-income mutual funds relative to Malaysia's fixed-income index (Markit iBoxx ALBI Malaysia Total Return Index).

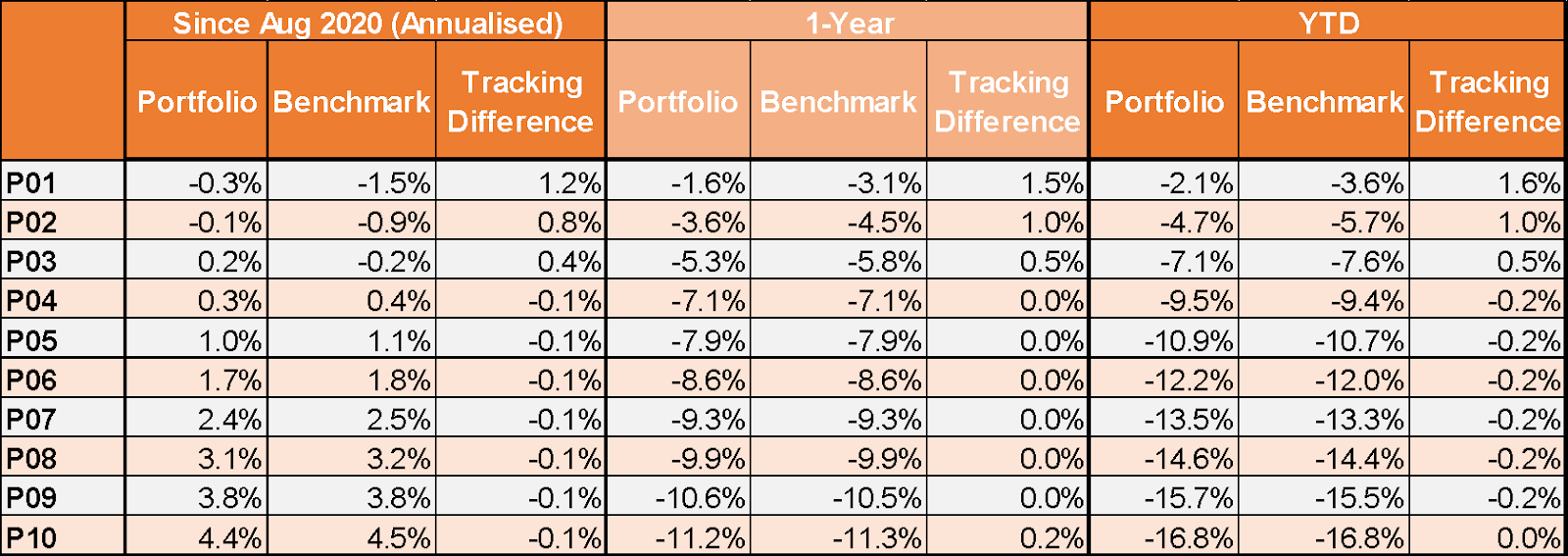

Total Returns in MYR

<Source: Morningstar>

The total returns were higher as Ringgit depreciated by 4.9% (Since Aug 2020), 9.8% (1-Year) and 9.9% against the USD.

Fear-Gripped Markets Could Present Long-Term Investment Opportunities

"I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful." — Warren Buffett

For most investors, volatility is an enemy. Volatility leads to fear; fear leads to panic; panic causes poor decision-making. Investors fear markets could easily fall further, inflation could persist, the recession could rage, or the war in Ukraine could worsen.

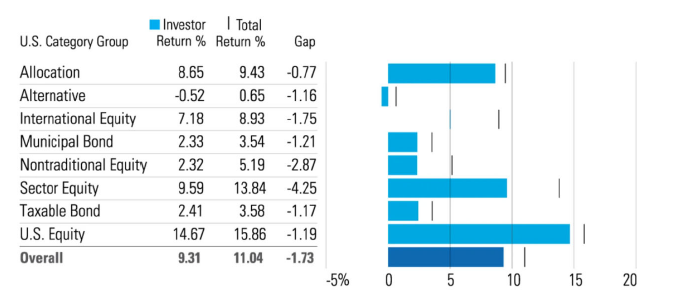

Morningstar's Annual "Mind the Gap" study highlights the difficulty in timing market entry and exit points. The "gap" refers to the shortfall between total and investor's returns or an investment's money-weighted returns, which adjusts for asset flows. The data consistently show that investors mistime their purchases and sales, as indicated below:

The Gap by US Category Group (10-Year Returns)

<Source: Morningstar, Data as of 31 December 2021. Excludes commodities category group. Gap numbers may not match differences in returns because of rounding.>

The research study also suggests that investors can improve their investment returns by:

• holding a small number of widely diversified funds;

• automating routines like rebalancing;

• avoiding narrow or highly volatile funds; and

• embracing dollar-cost averaging techniques.

In addition, down markets often present opportunities and offer better value for patient investors in the long term.

Disclosures

Past data and performance do not indicate future performance. Actual individual investor performance will vary depending on the initial investment, amount and frequency of contributions, allocation changes, taxes and fees during the time frame considered